CES: Live Coverage From My Living Room

Lots of CTV, tons of AI and a spoon of Fun

Welcome back to Streaming Made Easy (SME). I’m Marion & this is your 5-min read to get a European take on the Global Streaming Video Business.

Every Friday in your inbox. Check out previous editions here.

Enjoy today’s read.

ICYMI 🔥

Netflix added 8M Global Monthly Active Users to its ad tier in 2 months (totalling 23M now) and 85% of them spend 2 hours a day on the service. Still missing some context here. How about on average across all plans? If you pay less, do you watch more or less feeling less pressure to make the most of your subscription price?

GroupM wants innovative and scalable ad formats and teams up with a blend of big media, CTV and digital outlets to that end. The goal? Increased engagement and in turn more $$.

Lupin Part 3 makes Netflix’s Most Watched List 🐓 🇫🇷

I wrote today’s piece from the comfort of my living room as I didn’t make the trip to CES.

Let’s make it a 2025 goal though.

Until then, here’s what grabbed my attention remotely.

Today at a glance:

The CTV Corner

The AI Corner

The Fun Corner

The Press Conference Corner

Let’s dig in:

The CTV Corner

In a decade, Streaming services have revolutionised the way we consume content, offering unparalleled convenience and a vast array of choices.

As the Streaming landscape expands, the importance of a seamless and user-friendly TV operating system has grown exponentially.

Two sets of players fight to stay or become the gatekeepers of your living room: Pay TV and Connected TV.

In my “Battle for the living room” Series, I aimed to provide a comprehensive analysis of the CTV OS market, examining the strategies and innovations behind each player's approach to capturing a slice of this lucrative market.

Check out the entire Series here.

CES 2024 took place this week and it brought me to ask the question: who's winning the TV OS wars?

No one yet.

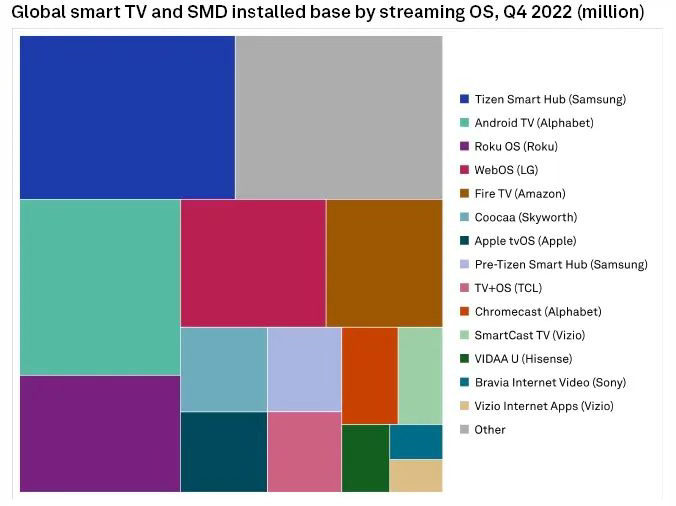

This is what the ecosystem looked like in 2022 according to Research Company S&P Global:

I’m eager to see 2023 numbers especially with:

Hisense maintaining its n°2 spot in terms of TV shipments (note that Hisense TVs are powered by their own OS Vidaa but also Android TV or Roku depending on the TV model).

“Vidaa is the most growing OS in Europe!!! We grew more than 100%YOY and reach 11% market share we believe by end of the year we will be 13% with more than 15 brands all over Europe. We are aiming next year for 20% market share.” - Guy Edri, CEO Vidaa International (IFA 2023).

Roku launching its own set of TVs.

Samsung and LG opening the doors to their OS to other OEMs.

It won’t show us a clear winner though and 2024 will be no different.

Actually 2024 will bring even more fragmentation with:

Comcast's Entertainment OS coming to more devices via Xumo

Sonos rumoured to get into the streaming box business

ZEASN ready to go bigger after its Foxxum acquisition

TiVo in the starting blocks for a wider roll out

Amazon Fire TV breaking free from Google

Vizio looking to license WatchSmart

CES is the perfect opportunity to understand what’s coming in 2024 and here’s what happened:

→ The TCL & Roku & Google TV Trio

I often read that TCL made Roku the n°1 TV OS in the US except it’s not how partnerships work.

Roku too made TCL who they are today: the n°2 TV seller in the US.

Prior to their partnership in 2014, Roku was only powering streaming dongles, TCL ranked n°6.

Now, back in 2020, TCL decided to go with Google for a set of TV models. My take:

1/ It was a way to mitigate the over-reliance on one OS partner.

2/ Google must have made them a sweet licensing proposal.

More TVs will be powered by Google this year (as announced at CES) and yes it is a blow to Roku which may explain why they now make their own TVs too.

Is it the final axe? Not yet.

In the US, think of the millions of TVs still active.

Outside of the US, the pair still works together e.g. 8 models in store in the UK.

Finally, Roku has other OEM partners, granted they’re not TCL ot Hisense.

→ The risk of a Chromecast feature on LG

Funny enough, I made use of that feature on a Samsung device in a hotel last week.

From a user standpoint, I was thrilled to find this feature as TVs in hotels are from smart (at least in Europe).

From LG’s standpoint, I’m not sure I get the move though. The user circumvents their UI which means: missed opportunities to show banner ads, drive engagement hours and claim a cut on potential on platform sign ups.

Maybe Google pays a license fee per active device to LG but I see this as a risky move long term. Next up, will LG TVs be powered by Google TV?

→ Samsung gets tighter with its customers

I suspect this move follows the creation of the Kids hub. You offer a safe space for kids and brands alike. It’s no secret that monetisation of made for kids content is challenging on CTVs.

Now will it also provide value to viewers via recommendations, quicker content discovery and boost time spent?

Will it give Samsung more insights into its users? If so, combined with ACR data = 🔥

In any case, it shows that Samsung understands it needs to build a customer relationship beyond the one off sale of a TV.

→ Turnkey solution for operators with TiVo Broadband

I wrote about Google’s edge in the OS wars with their operator tier value proposition.

They are years ahead of anyone else and so far the only ones who cracked the code. Many have given up either because of (too?) long sales cycles with Telcos or a segment proving to be too demanding with customisation and so challenging to scale.

TiVo Broadband empowers operators to deliver premium subscription video on demand (SVOD), TiVo+ Free Ad-Supported Television (FAST), and customer-specific linear channels to their broadband-only customer base. Operators can also choose to add a device to the mix with Evolution Digital’s EVO FORCE 1 and FUSE 4K stick.

Curious to see what this looks like in practice.

→ Other announcements include:

Pump up the volume with 3SS and Dolby

Gaming in cars with Ludium Lab, ACCESS Europe and XPENG

Two more partners for TiVo OS

Shoppable viewing experience with Telly and The Take

Only stopping by? Consider subscribing to receive it every Friday morning

Loving it? Consider sharing it with your network ❤️

The AI Corner

No surprise to see AI everywhere. However, a tiny bit more challenging to distinguish the buzzword (throughout coms and marketing materials) from the truly innovative implementations.

Three things caught my attention:

→ ChatGPT gets a body:

With Telly TVs and its “Hey Telly” voice command powered by ChatGPT. Amazon, Apple and Google poured billions in their voice assistant efforts. Will ChatGPT simply take over as THE brain behind voice assistants?

With Volkswagen Cars and again a ChatGPT integration.

A button on a Dell keyboard with Microsoft Copilot key for fast access to the AI assistant.

→ A step towards consent and compensation in AI?

A major concern from rights holders is the fact that technologies like ChatGPT use their copyrighted work without consent, nor compensation (a great example of the year ahead on this topic is the NY Times law suit against OpenAI) to train their large language models.

SAG-AFTRA, representing performers, signed an agreement with Replica Studios under which union members can license digital replicas of their voices for use in video games. Note that the agreement does not cover the use of performer voices to train LLMs though.

→ AI optimisations

Technology for the sake of technology is short lived.

Samsung seems eager to put AI to work for actual relevant use cases within our industry.

Check out Tobias Künkel’s post on Samsung's support for real-time AI subtitles or CNET’s piece on Samsung’s AI picture enhancement feature.

The Fun Corner

Who will buy this? No clue but it looks pretty darn cool.

If video embeds don’t work in your inbox, go here.

This is for the BBQ addicts out there. I know a few 😉

And Samsung’s Music Frame sure looks nice.

The Press Conference Corner

To go even deeper:

If video embeds don’t work in your inbox, go here.

If video embeds don’t work in your inbox, go here.

If video embeds don’t work in your inbox, go here.

If video embeds don’t work in your inbox, go here.

That’s it for today but before you go:

Enjoy your weekend and see you next Friday for another edition of Streaming Made Easy!

By night, I write Streaming Made Easy and on Linkedin.

By day, I run The Local Act, a streaming video consultancy.

Whenever you’re ready, there are 3 ways I can help you:

→ Europe Made Easy: Get a trusted partner to launch and grow in Europe.

→ Masterclasses: For executives looking to get up to speed on all things streaming. My “FAST Made Easy” masterclass has been in high demand.

→ Content Marketing: Explore how I can put my 5.9K LinkedIn following + my 3.6K Newsletter subs to work for your company like I do for mine.

I cater to Streamers, Distribution Platforms and Technology Vendors.

Ping me to see if we’re a fit.